What began as a freight and logistics shock has become something more serious for aluminium. The Gulf is no longer just a region facing disrupted trade flows. It is now a region dealing with impaired operating rates, damaged assets and a supply chain that has become harder to restart cleanly even if shipping conditions improve.

At a glance

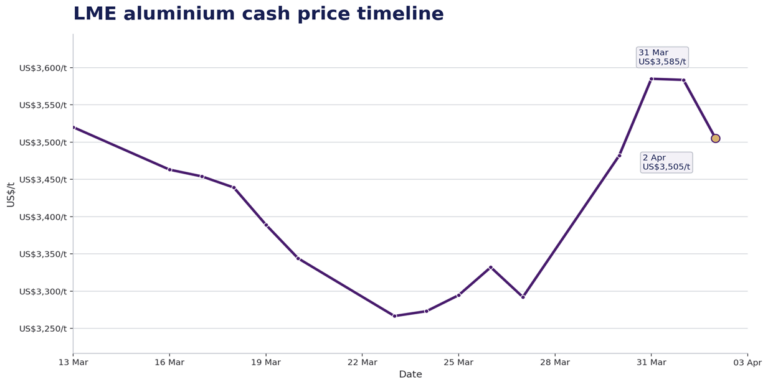

- LME aluminium cash reached US$3,585/t on 31 March 2026 and was still at US$3,505/t on 2 April, showing that the rally held even after the first phase of the shock.

- The problem has moved beyond shipping. Gulf aluminium assets have been damaged, major smelters are operating below normal rates and effective supply loss now looks more durable.

- The squeeze is being felt most acutely by Western buyers because the Gulf matters more in exportable non-Chinese aluminium than in total global smelting capacity.

- The next phase is more complicated. Aluminium is still dealing with a supply shock, but it now also faces a weaker macro backdrop as higher energy prices and slower growth begin to affect demand expectations.

Prices have moved from panic to persistence

The most striking feature of the aluminium market is not that it rallied. It is that it stayed high. On the LME, aluminium pushed up to US$3,585/t on 31 March, held at US$3,583.5/t on 1 April, and eased only modestly to US$3,505/t on 2 April. That still leaves the market comfortably above the mid-March level and well above the February low.

That kind of price behaviour tells its own story. Aluminium did not spike on headlines and then collapse once the immediate shock passed. It repriced and then held those gains. That usually means the supply problem is more persistent than first assumed. The issue is no longer whether disruption exists. The issue is how long it lasts, how much metal has already been lost and how much additional capacity may still remain at risk.

The physical market reinforces the same message. When the benchmark price stays high and physical premiums remain elevated at the same time, the market is signalling that the problem is not just fear on exchange screens. It is a tightening in real units available to consumers.

The story is no longer just about Hormuz

Hormuz is still central to the aluminium shock, but it is no longer the entire story. The market has had to absorb a move from blocked trade to damaged capacity. That is a more serious phase of the disruption because shipping delays can sometimes be worked around. Damaged plants and impaired operating systems are harder to normalise.

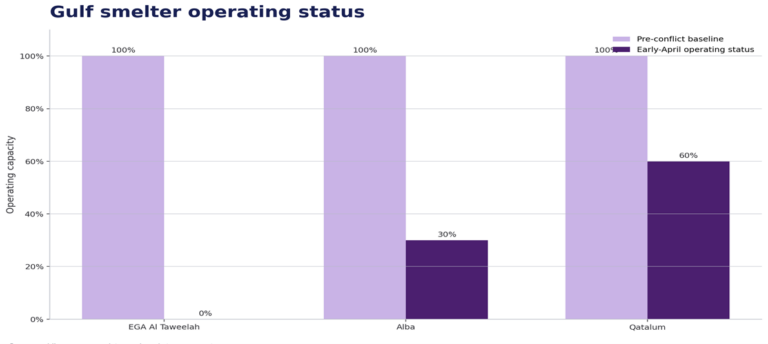

That change is most clearly visible in the Gulf operating base. One of the region’s most important aluminium hubs, EGA’s Al Taweelah complex, has suffered significant strike damage. Once a complex of that scale is impaired, the market stops thinking in terms of delayed exports and starts thinking in terms of slower recovery.

The operating picture has worsened

The Gulf aluminium system is now operating below normal in a more visible and more consequential way. Qatalum remains constrained at around 60% capacity, which means the market is still not receiving normal supply from one of the region’s major producers.

Alba’s position looks weaker still. What began as defensive curtailment has become a much more serious loss of effective operating capacity. Taken together, a damaged UAE complex, a heavily impaired Bahraini smelter and a still-constrained Qatari producer mean the market is not dealing with one isolated problem. It is dealing with multiple impaired assets across the same region, all sitting inside the same disrupted logistics and energy system.

Why the pain is concentrated in the West

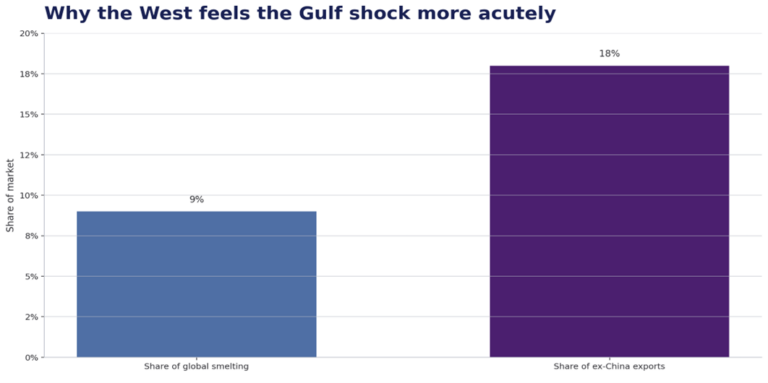

This is not simply a global aluminium shortage in the abstract. The Gulf matters because it is a disproportionately important source of exportable non-Chinese aluminium. The region accounts for about 9% of world smelting capacity, but around 18% of non-Chinese aluminium exports. That is the metric that explains why Europe and the US have felt the squeeze so quickly and so severely.

Total world output is not the same thing as accessible supply for Western consumers. What matters is how much flexible export metal remains available outside China, and that pool has tightened materially. Aluminium may still be abundant somewhere in the system, but the units that matter most to Western buyers have become harder to

access, harder to replace and more expensive to secure.

The supply story now looks more durable

In the early phase of the shock, it was still possible to imagine a relatively quick stabilisation if shipping reopened, gas supply improved and inventories were managed carefully. That view has weakened. Damaged assets imply repair time. Reduced operating rates imply lost tonnes. Disrupted trade routes imply ongoing friction even if some traffic resumes.

Commodity markets are usually comfortable absorbing short-lived interruptions. They become much more nervous when disruption stretches into an open-ended recovery period. That is where aluminium now sits. The concern is no longer just interruption. It is duration, and duration is what keeps prices high.

The macro backdrop is now part of the equation

The supply story is still dominant, but it is no longer the only story. Higher energy prices, slower growth and a wider inflation shock are now part of the aluminium equation. The market is balancing an ongoing supply squeeze against the possibility that prolonged energy stress starts to weigh on industrial demand, manufacturing activity and construction.

That does not remove the bullish supply case. It makes the path forward less one-directional. Aluminium can still remain tight and expensive, but it is now moving inside a broader macro environment that may eventually soften demand as well as strain supply.

Diplomacy may matter, but damage has already been done

Partial reopening, ceasefire discussion and negotiation headlines may improve sentiment at the margin, but they do not instantly reverse what has already happened to the aluminium supply chain. Smelters do not return to normal overnight. Damaged complexes do not rebuild immediately. Inventories do not replenish the moment shipping conditions improve.

That means the market is no longer dealing with a clean binary of disruption versus resolution. It is dealing with transition risk. Some corridors may reopen, some flows may resume and some operating rates may improve, but the aluminium system has already been altered. Recovery is likely to be uneven rather than immediate.

Aluminium is now trading on persistence, not surprise

The aluminium market is no longer reacting to surprise. It is reacting to persistence. Prices have stayed high because the underlying fears were not disproved. They were reinforced. Operating conditions worsened, the supply loss became more visible and the market started to recognise that the real shortage sits in exportable non-Chinese aluminium rather than in the global total.

That is why aluminium still looks like a geopolitical metal. The market is not merely responding to conflict. It is pricing the persistence of conflict-related damage across one of its most important export regions.

For now, vulnerability still matters more than resolution

Until operating rates recover, damaged assets are repaired and the corridor becomes reliably usable again, aluminium is likely to remain a market defined more by vulnerability than by resolution. The supply chain has already changed, and that keeps the premium embedded even if the geopolitical backdrop improves.

Aluminium remains the metal of transport, packaging, wiring, construction and electrification. But for now it is also trading as a geopolitical metal, one whose availability depends on whether Gulf production can stabilise, whether feedstock and energy supply can normalise and whether disrupted tonnes can be replaced quickly enough elsewhere.