For much of the past year Indonesian coal had been drifting lower. Then the Iran conflict rippled through oil and LNG markets, and the same old fuel-switching logic reasserted itself: when gas tightens and energy security becomes the priority, coal moves back into favour.

At a glance

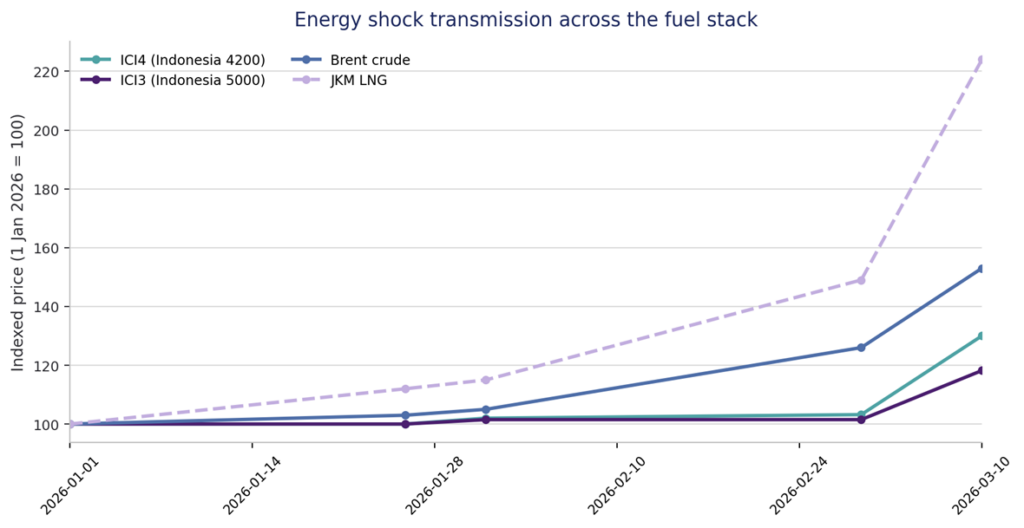

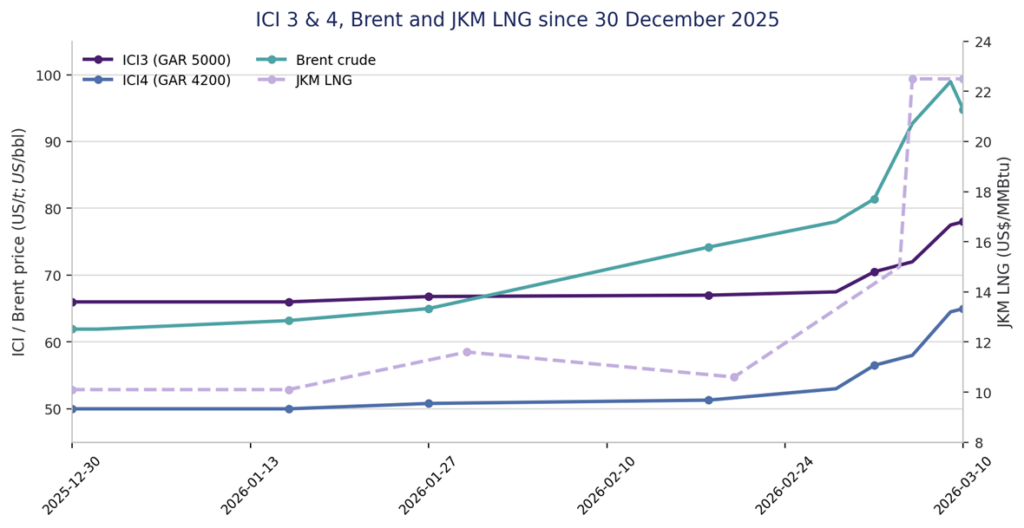

- ICI 3 rose from around US$67/t at the start of the period to about US$78/t, while ICI 4 climbed from roughly US$50/t to US$65/t.

- Brent crude moved from the low-US$60s/bbl at end December to over US$100/bbl at the height of the shock.

- JKM LNG jumped from around US$10/MMBtu in January to above US$22/MMBtu in early March.

- The price move was driven less by coal supply disruption than by the repricing of gas, freight risk and power-sector fuel switching.

A market that had been drifting

Before the Middle East shock, Indonesian coal was not a market attracting much urgency. Chinese domestic supply remained strong, Indian buying was selective, and low-rank Indonesian cargoes were widely available. Prices were soft, especially in the 4,200 and 5,000 GAR range that dominates the country’s seaborne trade.

That mattered because Indonesia sits at the flexible end of the thermal coal system. When power markets are calm, its lower-rank coal can look abundant and unexciting. But when utilities need fast-moving tonnes at short notice, Indonesian supply becomes the easiest balancing fuel to reach for.

The market therefore entered 2026 in a fragile equilibrium: oversupplied enough to feel comfortable, but still highly exposed to any shock that tightened the wider fuel stack.

Oil fires the opening shot

The first signal came from crude. As the conflict around Iran escalated and traders began to price the risk of disruption through the Strait of Hormuz, Brent moved sharply higher. The oil market was not reacting only to physical losses; it was responding to the possibility that one of the world’s key energy arteries could become harder and more expensive to use.

That mattered beyond oil itself. Once crude starts to reprice geopolitical risk, freight, insurance and broader energy sentiment move with it. Coal was not the first market to react, but it quickly found itself pulled into the same chain of repricing.

LNG tightens — and Indonesian coal becomes the fallback

The more important transmission channel was gas. Asian LNG buyers were already operating in a market with limited spare flexibility, and any perceived risk to Gulf cargoes immediately tightened prompt pricing. JKM surged, lifting the marginal cost of power generation across import-dependent markets.

When gas becomes both expensive and uncertain, coal regains competitiveness very quickly. That is especially true in Asia, where coal-fired capacity remains large and where Indonesian tonnes can move faster than most other seaborne alternatives.

The low-rank grades move first

That is why the lower-rank Indonesian indices moved so quickly. ICI 4, the benchmark for 4,200 GAR material, and ICI 3, the key 5,000 GAR grade, are precisely the products many buyers use when they need affordable replacement fuel rather than premium heat value.

The move was not about mines going offline or export routes from Indonesia being cut. It was a classic power-market response: gas tightened, utilities recalculated burn economics, and low-rank Indonesian coal was suddenly back in demand.

The shock spreads through the fuel stack

Viewed on an indexed basis, the move in Indonesian coal was part of a broader energy repricing rather than an isolated coal story. Brent and JKM moved first and further, but the coal indices followed in the same direction as the market translated geopolitical risk into higher marginal power costs.

That is a useful reminder of how thermal coal behaves in modern energy markets. It rarely leads the panic, but it often benefits once the initial shock in oil and gas starts to feed through into utility procurement.

Coal, oil and LNG move together again

The relationship is not one-to-one, and the commodities do not trade in the same units, but the direction of travel matters. ICI 3 and ICI 4 tracked higher alongside Brent, while JKM moved on a steeper axis altogether as Asian gas buyers scrambled to secure supply.

In other words, Indonesian coal was not rallying because coal fundamentals had suddenly become tight on their own. It was rallying because the wider fuel complex was repricing energy security.

Indonesia is the swing supplier

Indonesia occupies a unique position in this system. It is the largest seaborne exporter of thermal coal and the dominant supplier of lower-rank material into China, India and much of Southeast Asia. When buyers need prompt cargoes, Indonesian coal is usually the first pool of supply they test.

That proximity matters in a crisis. Shorter voyages, familiar specifications and a deep spot market give Indonesian coal an advantage when utilities are trying to respond quickly to volatility in gas and oil.

What happens next?

Whether the rally extends will depend less on Indonesia itself than on the persistence of the broader geopolitical premium. If Brent and LNG remain elevated, coal burn economics are likely to stay supportive and Indonesian prices may hold firm or move higher again.

But the reverse is also true. If shipping fears ease and gas markets normalise, Indonesian coal could give back some of its gains just as quickly as it found them. This remains a shock-driven rally, not a structural shortage story.

For now, coal still matters

For years the dominant narrative has been that coal’s role in power markets is steadily fading. Yet episodes like this show how quickly that story can be interrupted when energy security re-emerges as the overriding concern.

The Iran conflict has done exactly that. For a brief but telling stretch, the repricing of oil and LNG pulled Indonesian coal back into focus — and reminded the market that the old fuel still has a habit of returning when the system is under stress.